Summary

- Automotive loans of all types are on a downward trend in approvals, with a concurrent increase in interest rates

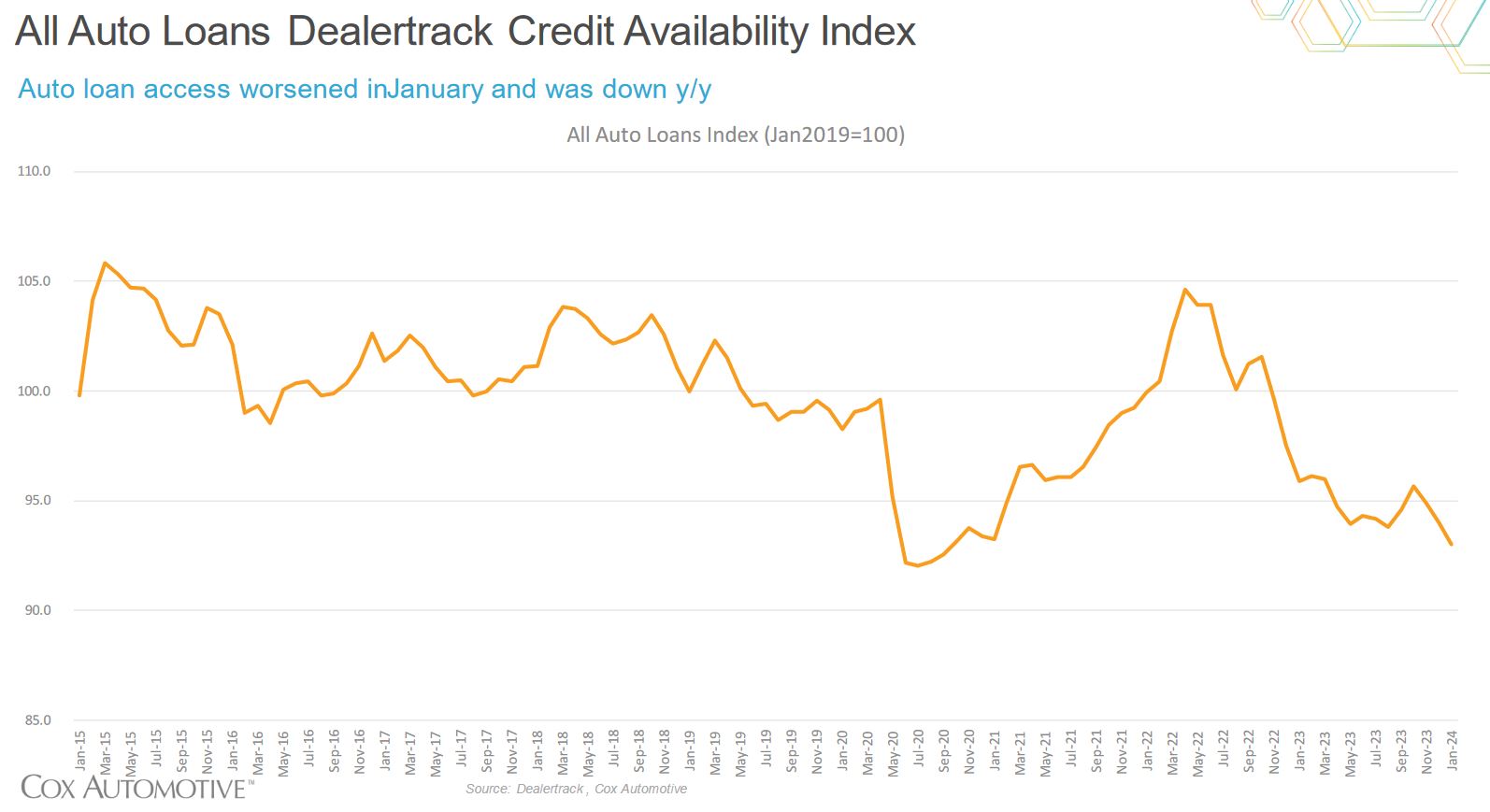

- The auto loan availability index has hit its lowest point in five years in January 2024 at 93%, compared to a baseline January 2019 100%

- Analysis of available date shows that there are four major factors driving this: Credit availability moving against consumers, approval rates decreasing overall, term lengths shortening with 72 month terms seeing the lowest approvals, and the tightening of alternative loan channels

- From the data, we believe there are a few options that can get a consumer a car this year, but all include some form of risk or acceptance of less-than-desirable interest rates

- Our analysis also shows that the trend might continue downward for a significant portion of 2024, so it may not be worth buying this year, new or used.

In the ever-changing landscape of automotive financing, access to credit plays a pivotal role in both driving vehicle sales through to signing on offers, as well as shaping overall consumer behavior. It is not understating the fact that securing auto credit can be the make-or-break part of any sale.

The January 2024 Dealertrack Credit Availability Index (CAI), as reported by Cox Automotive, provides an in-depth overview of the state of auto credit availability in the United States. The latest findings reveal a concerning trend of worsening credit availability, shedding light on the challenges faced by both consumers and industry stakeholders.

Year-to-Year Differences

Comparing data from January 2023 to January 2024, the Dealertrack CAI report highlights a notable decline in auto credit availability. This decline is reflected through several metrics, including overall credit approval rate and the share of prime and subprime borrowers.

That year-over-year credit approval rate has decreased by a significant 3%, signaling a tightening of credit standards by lenders. This, despite a recovering local economy in the USA and trade between the US and Canada normalizing close to pre-pandemic levels.

Additionally, there has been a shift in the composition of borrowers, with a decrease in prime borrowers and an increase in subprime borrowers, adding extra strain to the lending market. This has combined to cause the auto loan index to hit its lowest point since August 2020, coming in a full percentage point below that index.

Analysis

The decline in auto credit availability observed in the January 2024 Dealertrack CAI report warrants a closer examination of the underlying factors that are driving the trend. Several factors may be contributing to the tightening of credit standards by lenders:

- Credit Availability Factors Moving Against Consumers: In January, yield spreads widened on average by 15 basis points (BPs), the immediate effect of which was increasing rates on auto loans. Comparatively, the 5-year US treasury rate decreased by 2 BPs, driving the yield spread even wider.

- Approval Rates Decreasing Overall: The auto credit approval rate dropped 8 BPs in January 2024 alone, a 1.6% decrease compared to January 2023. Subprime shares also decreased to 11.2% in January 2024 compared to 11.4% in December 2023, despite the shares being up 0.6% year-over-year compared to December 2022.

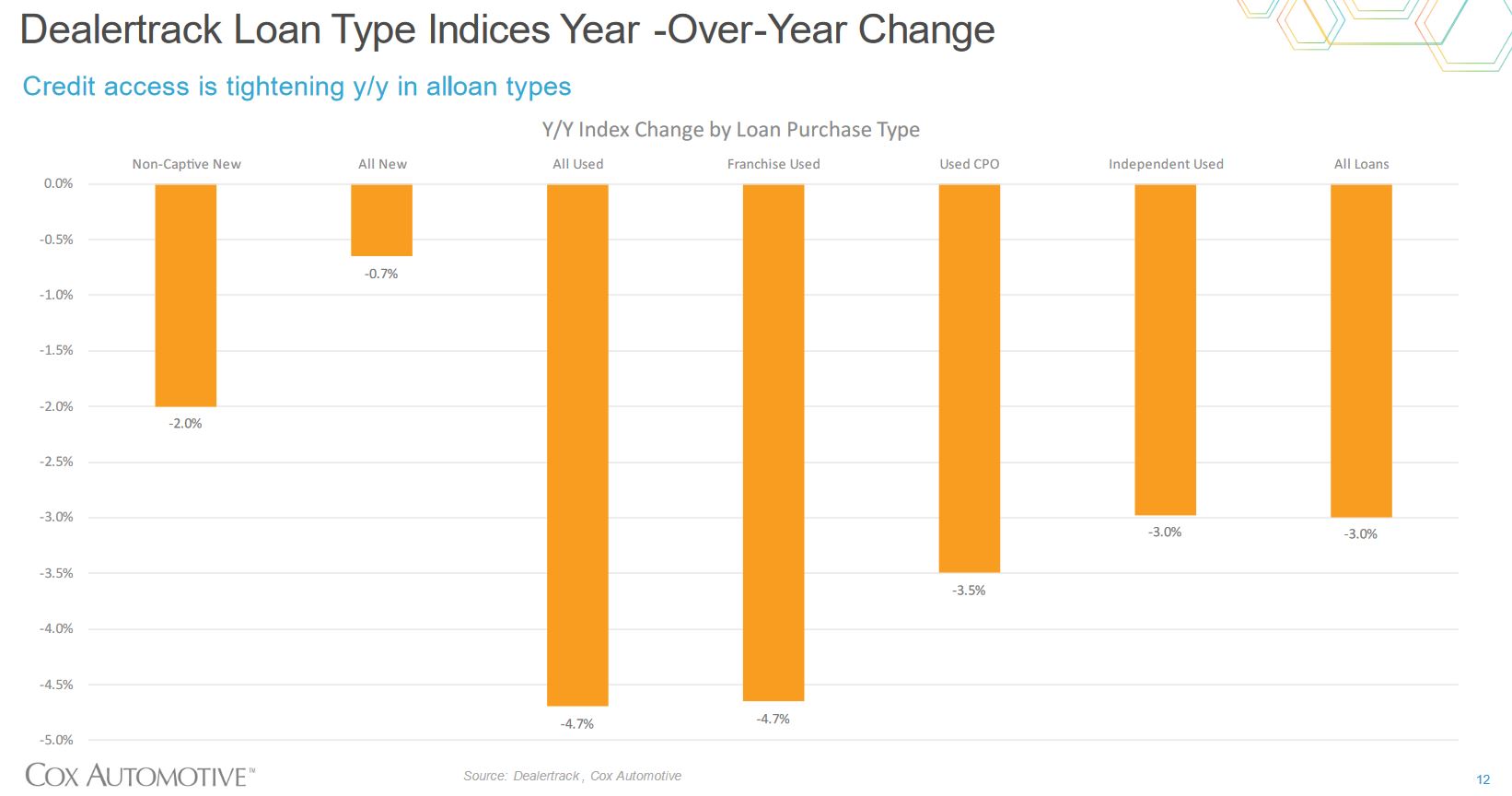

- Term Lengths Decreasing: To mitigate risk, auto credit lenders reduced the amount of approvals on long term loans, namely the 60 and 72 month terms. The share of loans in January decreased by 2 BPs, resulting in a 1.8% decrease year to year

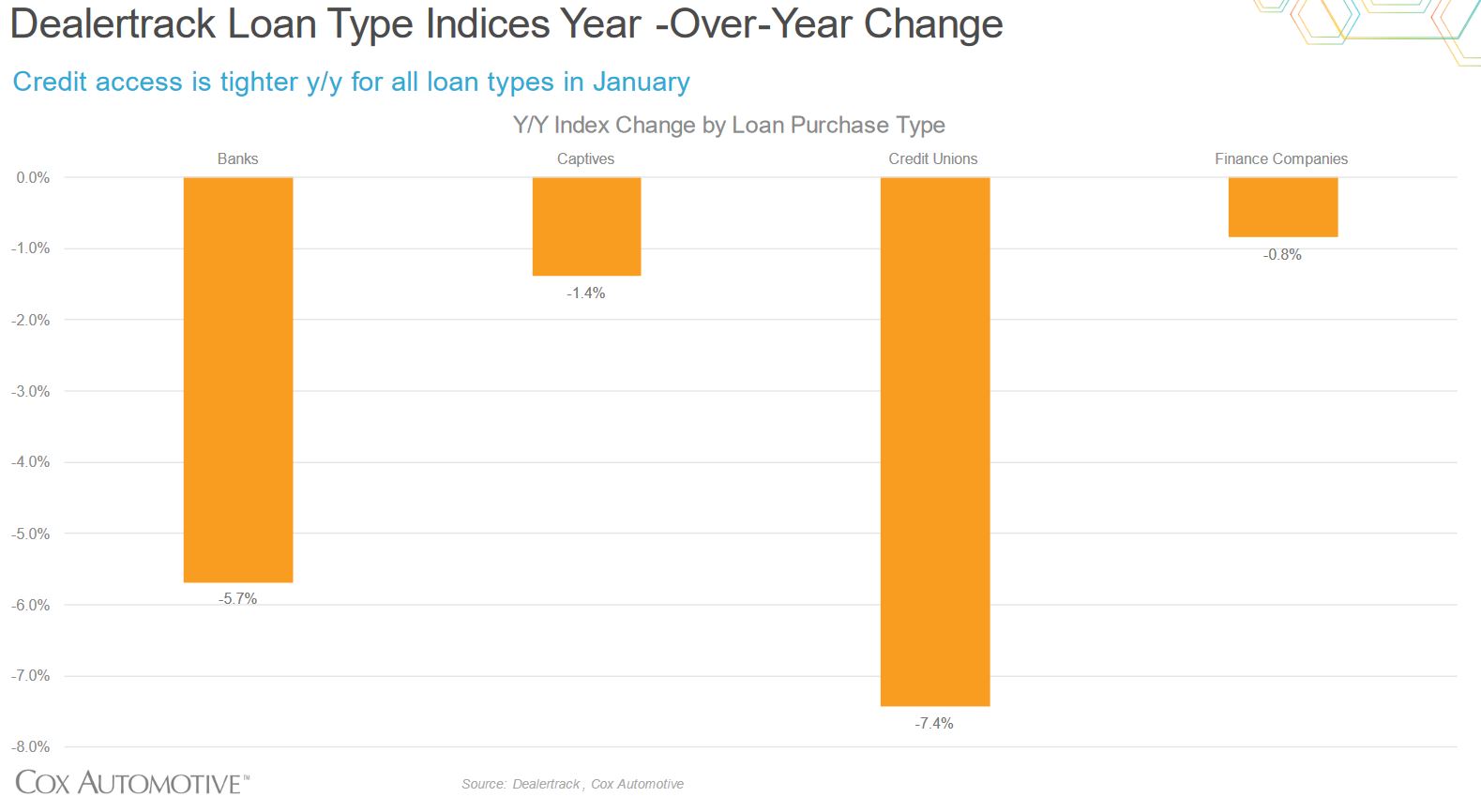

- All Loan Channels Tightening Approvals: It’s not just primary auto credit lenders feeling the pressure. Banks and independent credit unions tightened the most, restricting access to financing through alternate channels. In a year-to-year comparison, all credit types saw a significant shift in approval rates, sometimes by as 5.7% for banks and 7.4% for credit unions.

Overall Conclusions

The worsening of auto credit availability has significant implications for both consumers and industry stakeholders. For consumers, the tightening of credit standards has limited access to low rates for vehicle financing. Naturally, this is making it more difficult to purchase a new vehicle in 2024, especially for those with poor credit.

For industry stakeholders, including dealerships and automakers, the tightening of credit availability poses a significant challenge in driving vehicle sales and maintaining market momentum. Analyzing the available data, the base conclusion one can draw is that a decline in credit approval rates impacts sales volumes and profitability. This is particularly damaging to dealerships that rely heavily on OAC financing to ease the pressure of the sale and facilitate the movement of both new and especially used stock.

In our view the solution that we think will work best is to explore alternative financing options. This may include partnering with alternative lenders, or spreading the financing load across more than a single lender to reduce overall risk to each lender.

Some dealerships have also started offering flexible financing rates tied to the federal prime index (8.5% at the time of this writing), although this is mostly being used as a stopgap measure to keep sales up. It has little viability for long term use, especially with inflation creeping upwards as it has for the past three years.

Naturally, dealerships and automakers are wanting to focus on customer retention and loyalty, so another solution may be to offer incentives for accepting higher credit interest rates. These incentives could include providing all servicing covered for multiple years, or providing some options at no cost, as that cost will be recovered in the increased financing interest.

If those solutions do not work, the only other solution that presents itself is direct bank financing through a long-term loan with significant collateral such as home equity. Nevertheless, the current trend in auto credit approvals looks like it will get worse before it gets better, so for some it simply comes down to 2024 not being the year to buy a car.